Interest Rate Derivatives and Cross-Currency Applications

Interest Rate Parity (IRP) is one of the most important theories in finance. It links the interest rates, exchange rates, and expected returns on foreign exchange investments among different currencies. It is based on the idea that, in an efficient market, returns on equivalent assets denominated in different currencies should be equal when expressed in a common currency. IRP plays a crucial role in the foreign exchange markets and helps explain how interest rates and currency values are interconnected.

There are two main forms of interest rate parity:

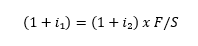

1. Covered Interest Rate Parity (CIRP):

Covered Interest Rate Parity arises when there is a possibility to eliminate currency risk through the use of forward contracts. In a covered interest rate parity scenario, the interest rate differential between two countries is equal to the forward premium or discount on the foreign currency. The formula for Covered Interest Rate Parity is as follows:

Where:

- i₁ = Domestic interest rate

- i₂ = Foreign interest rate

- F = Forward exchange rate

- S = Spot exchange rate

The equation indicates that, in a covered interest rate parity situation, the interest rate differential should be offset by the forward exchange rate premium or discount.

2. Uncovered Interest Rate Parity (UIRP):

Uncovered Interest Rate Parity assumes that investors are not able to eliminate currency risk through the use of forward contracts. Instead, it focuses on the relationship between spot exchange rates, interest rates, and expected future spot rates. The formula for Uncovered Interest Rate Parity is as follows:

Where:

- i₁ = Domestic interest rate

- i₂ = Foreign interest rate

- E = Expected future spot exchange rate

- S = Spot exchange rate

The equation implies that, in an uncovered interest rate parity situation, the interest rate differential is equal to the expected percentage change in the exchange rate.

Interest Rate Parity is a fundamental concept in international finance and is essential for understanding the relationships between interest rates and exchange rates.

Now let's move onto interest rate derivatives, starting with FX swaps.

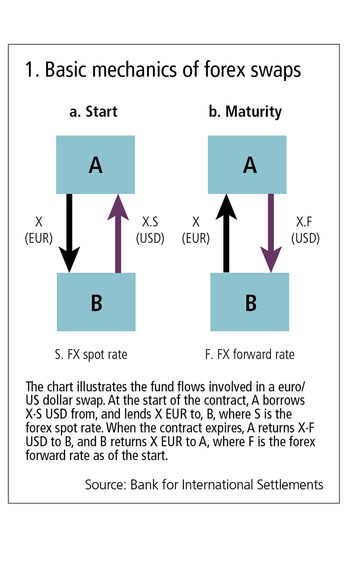

A Foreign Exchange (FX) swap is a financial derivative transaction that involves the simultaneous purchase and sale of identical amounts of one currency for another but with two different value dates. FX swaps are commonly used by market participants, including banks, financial institutions, and corporations, to manage currency exposure and liquidity needs.

The FX swap transaction consists of two legs:

1. Spot Leg:

In the spot leg of the FX swap, the parties involved exchange the principal amounts of the two currencies at the prevailing spot exchange rate. The spot exchange rate is the rate at which currencies can be traded for immediate delivery (typically within two business days).

2. Forward Leg:

In the forward leg, the parties agree to reverse the initial exchange at a predetermined future date and a pre-agreed forward exchange rate. The forward exchange rate is the rate at which currencies will be exchanged at the agreed-upon future date.

The primary purpose of an FX swap is to allow participants to manage their currency exposure while maintaining liquidity.

Here's how an FX swap works in practice:

- Party A needs a certain amount of currency X and has currency Y.

- Party B needs currency Y and has currency X.

- In the spot leg, Party A exchanges currency Y for currency X with Party B at the current spot exchange rate.

- Simultaneously, in the forward leg, Party A agrees to sell currency X back to Party B at a predetermined forward exchange rate at a specified future date.

- At the agreed-upon future date, the parties exchange the currencies again, completing the FX swap.

The key features of an FX swap include:

Net Cash Flow: In an FX swap, there is typically an initial exchange of currencies, but the net cash flow is settled at the maturity of the forward leg. The net cash flow is calculated based on the difference between the initial exchange rate and the forward exchange rate.

Maturity Dates: The maturity date of the forward leg is determined at the outset of the transaction and can vary depending on the needs of the parties involved.

Interest Rate Differential: FX swaps may involve an interest rate differential between the two currencies, reflecting the cost of carrying the positions over the swap period.

The formula for calculating the net cash flow or settlement amount in an FX swap depends on the interest rate differential between the two currencies involved in the swap. The net cash flow is determined at the maturity date of the swap and is based on the difference between the initial spot exchange rate and the agreed-upon forward exchange rate. The formula can be expressed as follows:

Where:

- P is the principal amount of the swap.

- r₁ is the interest rate of the currency being bought (in decimal form)

- r₂ is the interest rate of the currency being sold (in decimal form)

- t₁ is the number of days to the maturity date of the spot leg, typically expressed on a 360-day basis

- t₂ is the number of days to the maturity date of the forward leg, typically expressed on a 360-day basis

- F is the agreed-upon forward exchange rate

- S is the initial spot exchange rate

The calculation involves two components:

- The present value of the principal amount converted at the interest rate of the currency being bought.

- The difference between the present value of the principal and the forward contract's notional value, which represents the agreed-upon exchange rate.

FX swaps are widely used for various purposes, including hedging currency risk, managing cash flows, and obtaining funding in different currencies. They provide flexibility to market participants in handling currency positions over different time frames while minimizing exposure to exchange rate fluctuations.

Similar to FX swaps, let’s explore interest rate swaps, which help manage interest rate risk.

An Interest Rate Swap (IRS) is a financial derivative contract between two parties that involves the exchange of interest rate cash flows over a specified period. In an interest rate swap, the two parties agree to exchange interest payments in order to manage or hedge exposure to interest rate fluctuations. This type of derivative allows entities to customize their interest rate profiles and effectively manage their interest rate risk.

The most common form of an interest rate swap involves exchanging fixed-rate interest payments for floating-rate interest payments or vice versa.

There are two main legs in an interest rate swap:

· Fixed Leg: One party agrees to pay a fixed interest rate on a notional principal amount over the life of the swap. The fixed interest rate is predetermined at the initiation of the swap and remains constant throughout the swap's term.

· Floating Leg: The other party agrees to pay a variable (floating) interest rate based on a reference interest rate index, such as the London Interbank Offered Rate (LIBOR) or the Euro Interbank Offered Rate (EURIBOR). The floating rate is reset periodically according to the terms of the swap agreement.

The key features of an Interest Rate Swap include:

· Notional Principal Amount: The notional principal amount is the hypothetical amount used to calculate interest payments but is not actually exchanged between the parties. It determines the cash flow amounts but does not represent a debt or asset.

· Payment Frequency: Interest rate swaps can have different payment frequencies for the fixed and floating legs, such as quarterly, semi-annually, or annually.

· Maturity Date: The maturity date is the agreed-upon date when the interest rate swap contract terminates, and any final settlement occurs.

Interest rate swaps are commonly used for various purposes, including:

· Interest Rate Risk Management: Entities use interest rate swaps to manage exposure to interest rate fluctuations. For example, a borrower with a variable-rate loan may enter into an interest rate swap to convert the variable-rate payments into fixed-rate payments.

· Speculation: Traders may use interest rate swaps to speculate on the direction of interest rates, hoping to benefit from favorable rate movements.

· Asset-Liability Management: Financial institutions use interest rate swaps to align the interest rate characteristics of their assets and liabilities, reducing interest rate risk.

· Customization: Interest rate swaps offer flexibility, allowing parties to customize their interest rate exposure to meet specific financial goals or requirements.

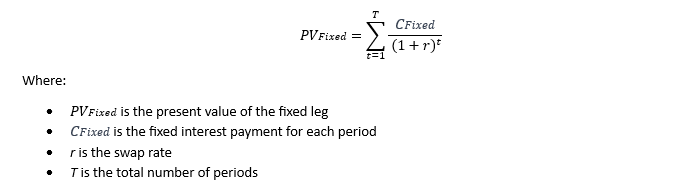

The valuation of an interest rate swap involves calculating the present value of future cash flows exchanged between the two parties.

The formula for the present value of the fixed leg of an interest rate swap (assuming fixed-rate payments) is as follows:

The formula calculates the present value of each fixed interest payment over the life of the swap, discounted at the swap rate. The sum of these present values represents the total present value of the fixed leg.

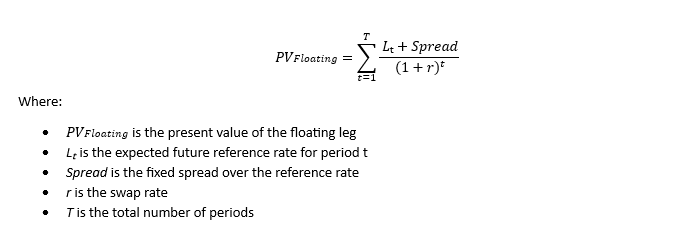

For the floating leg (assuming payments are based on a reference rate plus a spread), the present value formula is more complex due to the variability in the cash flows. It involves projecting future cash flows based on expected future reference rates and discounting them to their present value. The formula for the present value of the floating leg can be expressed as:

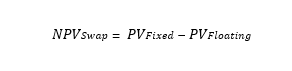

In practice, traders and financial analysts often use financial software or spreadsheets to perform these calculations. Additionally, the net present value of the swap is the difference between the present values of the fixed and floating legs:

This net present value represents the estimated fair value of the interest rate swap. Keep in mind that these formulas simplify the calculations, and various factors, such as day-count conventions and payment frequency, may affect the actual valuation.

Finally, let's look at cross-currency swaps, which combine elements of FX swaps and interest rate swaps.

A Cross Currency Swap (CCS) is a financial derivative in which two parties exchange cash flows in different currencies over a specified period. The primary purpose of a cross-currency swap is to hedge or manage exposure to currency risk, allowing entities to obtain funding in one currency while making payments in another.

In a cross-currency swap, there are two main legs:

- Principal Exchange: At the initiation of the swap, the two parties exchange principal amounts in different currencies. The principal amounts are typically notional, meaning they are used for calculation purposes but are not physically exchanged.

- Interest Rate Payments: Throughout the life of the swap, the parties make periodic interest rate payments to each other based on the agreed-upon notional amounts and interest rates. The interest rates can be fixed or floating, depending on the terms of the swap.

Benefits of a Cross-Currency Swap

The structure of a cross-currency swap allows entities to achieve specific objectives:

- Currency Conversion: One party may use the cross-currency swap to convert a liability denominated in one currency into a liability in another currency. This is useful when a company has operations in multiple currencies and wants to match its liabilities with its revenue streams.

- Foreign Exchange Risk Management: Companies with exposure to foreign exchange risk can use cross-currency swaps to hedge against adverse movements in exchange rates. By locking in a fixed exchange rate, entities can mitigate the impact of currency fluctuations on their cash flows.

- Funding in Different Currencies: Entities may use cross-currency swaps to obtain funding in a currency that offers favorable interest rates while making payments in a different currency. This can be advantageous when one currency provides a cost advantage in terms of borrowing costs.

The Pricing of a Cross-Currency Swap.

The pricing of a cross-currency swap involves calculating the present value of future cash flows in each currency, considering the exchange rate movements and interest rate differentials. The parties involved may agree on a fixed exchange rate for the principal exchange or allow for periodic adjustments.

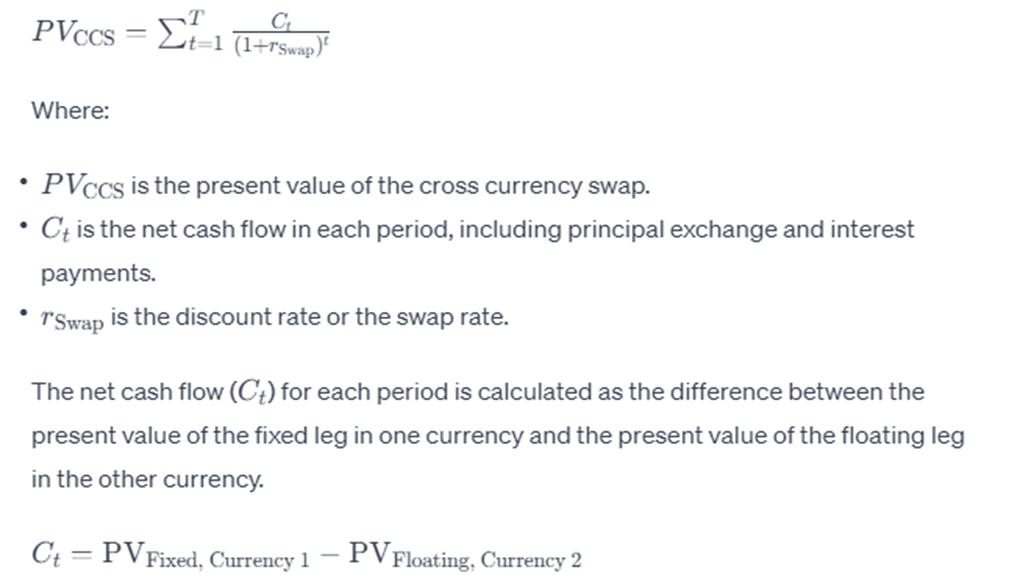

The general formula for the present value (PV) of a cross-currency swap is:

In practice, the calculation involves determining the present value of each future cash flow in both currencies, considering the relevant interest rates and exchange rates. This requires discounting each cash flow back to its present value using the appropriate discount factors.

In summary, interest rate derivatives, including FX swaps, interest rate swaps, and cross-currency swaps, are essential tools for managing interest rate and currency risks. Uncovered interest rate parity is a concept that explains the relationship between interest rates and exchange rates in foreign exchange markets. FX swaps are used to hedge currency exposure, while interest rate swaps are used to exchange cash flows at different interest rates. Cross-currency swaps combine elements of FX swaps and interest rate swaps to manage both interest rate and currency risks simultaneously. Understanding interest rate derivatives and cross-currency swaps is crucial in investment decision-making processes. By comprehending these concepts, investors can make informed decisions about their investment strategies.